Overview

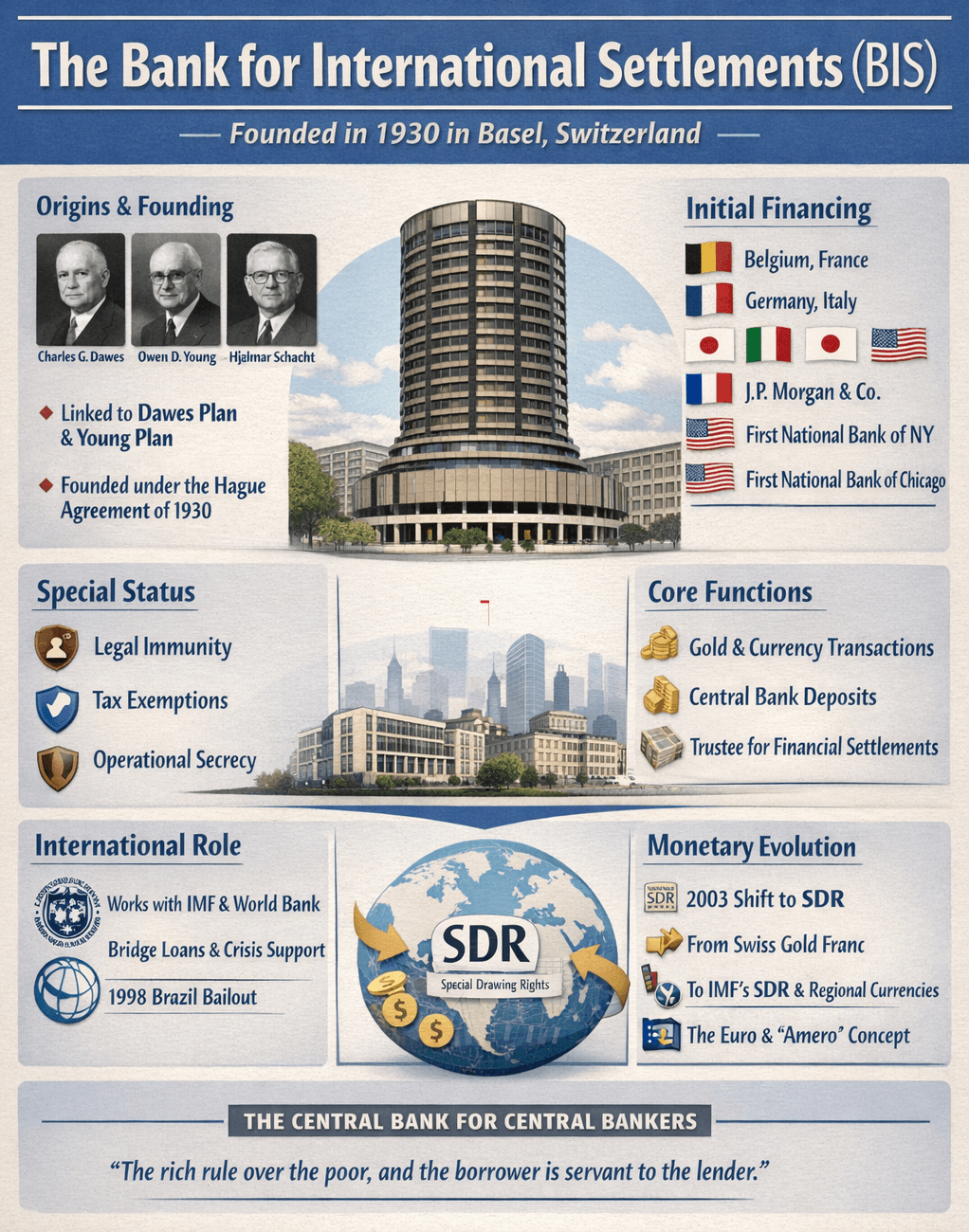

The Bank for International Settlements (BIS) was founded in 1930 during a period of severe political and economic instability following World War I. Its creation is tied to the international reparations system that emerged after the Treaty of Versailles in 1919, which imposed a heavy reparations burden on Germany. Charles G. Dawes, Owen D. Young, and Hjalmar Schacht were the principal figures connected to the BIS’s formation. Dawes, an American banker and politician, led the Allied Committee of Experts in 1924 and helped shape the Dawes Plan, which arranged for large foreign loans to Germany in an effort to stabilize its economy. Owen D. Young later replaced Dawes and advanced the Young Plan, which expanded and strengthened the earlier reparations framework. Hjalmar Schacht, head of the Reichsbank, is identified as the person who first proposed the idea of the BIS itself.

The BIS was formally established through the Hague Agreement on January 20, 1930. The agreement involved the governments of Germany, Belgium, France, the United Kingdom, Italy, Japan, and Switzerland. Switzerland agreed to grant the BIS a constituent charter with force of law and pledged not to alter that charter except in agreement with the other signatory governments. The institution was headquartered in Basel, Switzerland. Its stated purpose was to promote cooperation among central banks, provide additional facilities for international financial operations, and act as trustee or agent in international financial settlements.

At its founding, the BIS was financed by the central banks of Belgium, France, Germany, Italy, Japan, and the United Kingdom. Each central bank subscribed to 16,000 shares. Although the U.S. Federal Reserve did not join, three American private banks also participated and each received 16,000 shares: J.P. Morgan & Company, First National Bank of New York, and First National Bank of Chicago. In 2001, BIS ownership was restricted to central banks after a repurchase of privately held shares. At that time, 13.7 percent of the shares were still in private hands, and the BIS bought them back for more than $724 million at $10,000 per share.

The BIS is described as having extensive legal protections and institutional independence. Its buildings and surrounding grounds are treated as inviolable, and Swiss public authorities may not enter them without the bank’s consent. Its archives, records, and data are also inviolable. The BIS itself is granted immunity from criminal and administrative jurisdiction unless that immunity is formally waived. Its deposits, claims, and issued shares are protected from seizure or compulsory execution without prior agreement. Directors are described as enjoying immunity from arrest or imprisonment except in flagrant criminal cases, protection for their personal baggage, inviolability of papers and documents, immunity for acts performed in the course of duty, and exemptions from immigration restrictions. Employees are also described as exempt from Swiss taxes on BIS-paid salaries and protected from jurisdiction for acts carried out in the discharge of their duties. These protections were later reaffirmed in the 1987 Headquarters Agreement between the BIS and the Swiss Federal Council.

The BIS’s day-to-day functions are broad. Its statutes authorize it to buy and sell gold coin and bullion, hold gold reserves, accept supervision of gold for central banks, make advances to or borrow from central banks against gold and other approved securities, discount and rediscount bills of exchange and other short-term obligations, buy and sell foreign exchange, buy and sell negotiable securities other than shares, maintain deposit accounts for central banks, and accept deposits connected to trustee agreements involving governments and international settlements. It may also act as agent, correspondent, or trustee for central banks in international settlements. At the same time, it is not permitted to accept deposits from private individuals or corporations, and it may not make advances directly to governments or maintain current accounts in their names.

Decision-making at the BIS is described as resting with a board made up of the heads of certain member central banks. The board meets at least six times each year in secret. At these meetings, BIS management briefs the directors on financial operations, and global monetary policy is discussed and set. The board listed in includes central bank figures from Amsterdam, Frankfurt, Rome, Ottawa, Tokyo, New York, Washington, London, Paris, Stockholm, Brussels, and Zürich. Five members—representing Canada, Japan, the Netherlands, Sweden, and Switzerland—are elected by shareholders, while most directors serve ex officio.

The relationship between the BIS, the IMF, and the World Bank is described as a division of roles within international finance. The IMF deals directly with governments and lends money to countries in fiscal or monetary crisis, financing itself through quota contributions from member countries. The World Bank also lends to countries through its institutions, especially the IBRD and IDA, and raises money through direct bank lending and bond issuance. The BIS, by contrast, works with central banks and facilitates the movement of money between them. One of its known functions is the issuance of bridge loans to central banks when IMF or World Bank funds have been pledged but not yet delivered. Governments then repay those bridge loans when the promised international funds arrive.

The 1998 Brazil currency crisis is presented as an example of this wider system in operation. Brazil had accumulated heavy interest burdens on loans made over an extended period by banks such as Citigroup, J.P. Morgan Chase, and FleetBoston. In response, the IMF, the World Bank, and the United States assembled a large bailout package. Bernard Sanders criticized the bailout, arguing that it benefited large banks more than ordinary people and amounted to corporate welfare funded by taxpayers. His statement also criticized IMF-backed economic policies such as free trade liberalization, privatization, deregulation, and cuts to public spending, arguing that these measures harmed low-income and middle-class populations while helping corporations.

A major monetary change occurred on March 10, 2003, when the BIS abandoned the Swiss gold franc as its unit of account and adopted the IMF’s Special Drawing Rights (SDR). The SDR is described as an international reserve asset created by the IMF in 1969 to supplement official reserves. It is allocated to countries based on IMF quotas and serves as a unit of account for the IMF and some other international organizations. Its value is based on a basket of major currencies, identified as the euro, Japanese yen, pound sterling, and U.S. dollar.

The move from the gold franc to SDRs is presented as part of a broader development toward regional and possibly global currency systems. The SDR is described as a first step toward a stable and permanent international currency. The BIS is also described as having played an important role in the launch of the euro in Europe. Discussion of possible regional currencies extends to North America, where BIS Papers No. 17 is cited as noting that a NAFTA dollar, or “Amero,” had been proposed by some Canadian academics in light of the close trade relationship among Canada, Mexico, and the United States. The suggestion is that, just as the euro emerged within the European Union, a similar regional currency structure could theoretically develop in North America. C. Fred Bergsten’s description of the euro is a major surrender of national sovereignty to a supranational central bank.

The overall conclusion drawn is that the BIS occupies a central position in the international banking system. It is described as the central bank for major central banks, privately owned by central banks that are themselves largely private in nature, founded in controversial circumstances, protected by extraordinary secrecy and legal immunity, able to obscure the movement of money through its agency functions, and positioned to support the development of regional currency blocs and broader international financial integration. The concluding line emphasizes the relationship between debt and power with the quotation, “The rich rule over the poor, and the borrower is servant to the lender.”